Welcome Home

Helping Families Live Better Through The Best Home Financing

If you happen to come across another improved rate or cost option, we will make sure we do everything we can to match that offer. We don’t want you to sacrifice quality to get a better deal.

How it works: Request a copy of an official Loan Estimate from that company and send in that information and with your application details dated the same day, and we will be sure to go to bat for the best deal possible. If we can’t match the quote, well, we want what’s best for you and your family so if that’s the case we’ll be sure to make sure you’re taken care of until closing and that they honor that rate for you.

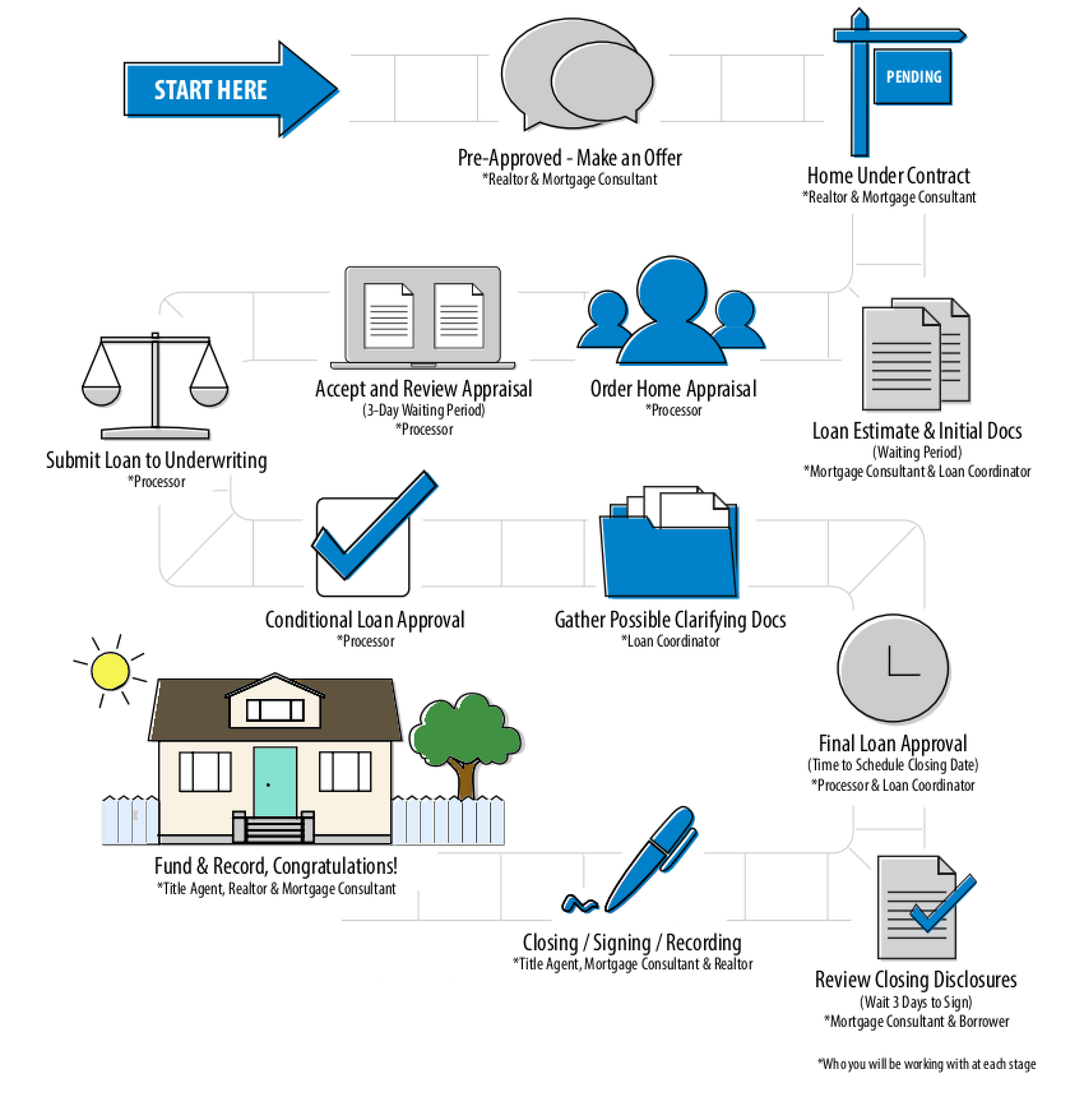

Pre-Approved – Make an Offer:

At this stage you will be working with your Realtor and Mortgage Consultant. The Mortgage Consultant will be taking your loan application and request documents from you in order to “pre-approve” your loan. Having a pre-approval letter will allow you to make offers on a home with your Realtor. This letter holds more weight with the seller because they see your offer is legitimate and you have the financing to back it up.

Offer Accepted! – Home Under Contract:

At this point you have received an accepted offer and you are now under contract for the home you are going to purchase. Your Realtor will disclose a copy of the accepted contract to the Mortgage Consultant. The Mortgage Consultant will then prepare your file to go into processing. Your Mortgage Consultant may contact you at this point for any clarifying information to go with your loan file.

Sign Initial Loan Documents:

Your Mortgage Consultant will let you know once your initial loan documents ordisclosures are ready for you to sign. You can sig n your initial loan documents in the office with us or we can send them to you via email or standard mail. Once you have signed these documents, your Mortgage Consultant can look into locking your interest rate.

Order Home Appraisal:

Your appraisal will be ordered by your Loan Processor. The appraisal fee is paid by you up frontoutside of closing costs on most loans. The Processor can order the appraisal as soon as signed disclosures are received.

Accept and Review Appraisal:

After your appraisal is completed you will receive an email from the appraisal network where you will be able to consent to eDelivery of the appraisal, download the authorization code, enter the code and then view the appraisal report.

Submit Loan to Underwriting:

At this time, your Loan Processor will prepare all your loan documents and submit them to the Underwriter for review. An Underwriter is a person who reviews the loan file for approval. They may need additional clarifying documents or explanations of items prior to approval. This process can take anywhere from three to five business days.

Conditional Approval:

Once the Underwriter has completed the review of your file, the Mortgage Consultant will receive a conditional approval. A conditional approval means your loan is approved subject to satisfying conditions (clarifying documents – see next step for more detail).

Based on the Underwriter’s conditions, your Mortgage Consultant may need your help with gathering some additional documents for the Underwriter to review. For example, the Underwriter may request a letter of explanation for a specific item, an updated bank statement, paystubs, additional signatures, etc. Your Processor will reach out to you if any additional items are needed.

Final Loan Approval:

Once your Processor has gathered all of the clarifying documents requested, they will submit them to the Underwriter for final approval. When the Underwriter gives final approval the Mortgage Consultant a clear to close, which means your loan can now close! At that time, your Processor will make arrangements with you and your Realtor to sign your closing documents at the Title Company.

Review Closing Disclosures:

You will need to review the closing disclosures 3 days prior to your closing and signing on the mortgage. Once you receive and review your closing documents, we must wait those mandatory 3 days before you are able to close.

Closing / Signing:

Your final loan closing usually takes place at a Title Company with a Title Agent present to assist you with your documents. A closing can also be arranged to have loan documents signed remotely with a mobile notary. Your Realtor and Mortgage Consultant may attend your closing and help answer any questions you may have.

Fund & Record:

After you sign, it takes about 24-48 hours for your loan to fund and record. Your Processor will be working closely with the Lender and Title Company to ensure every “t” is crossed and every “i” is dotted. Once the loan has funded and recorded, you will receive your keys from the Realtor and can move into your new home. CONGRATULATIONS, you own a home!

At this stage you will be working with your Realtor and Mortgage Consultant. The Mortgage Consultant will be taking your loan application and request documents from you in order to “pre-approve” your loan. Having a pre-approval letter will allow you to make offers on a home with your Realtor. This letter holds more weight with the seller because they see your offer is legitimate and you have the financing to back it up.

At this point you have received an accepted offer and you are now under contract for the home you are going to purchase. Your Realtor will disclose a copy of the accepted contract to the Mortgage Consultant. The Mortgage Consultant will then prepare your file to go into processing. Your Mortgage Consultant may contact you at this point for any clarifying information to go with your loan file.

Your Mortgage Consultant will let you know once your initial loan documents or disclosures are ready for you to sign. You can sign your initial loan documents in the office with us or we can send them to you via email or standard mail. Once you have signed these documents, your Mortgage Consultant can look into locking your interest rate.

Your appraisal will be ordered by your Loan Processor. The appraisal fee is paid by you up front outside of closing costs on most loans. The Processor can order the appraisal as soon as signed disclosures are received.

After your appraisal is completed you will receive an email from the appraisal network where you will be able to consent to eDelivery of the appraisal, download the authorization code, enter the code and then view the appraisal report.

At this time, your Loan Processor will prepare all your loan documents and submit them to the Underwriter for review. An Underwriter is a person who reviews the loan file for approval. They may need additional clarifying documents or explanations of items prior to approval. This process can take anywhere from three to five business days.

Once the Underwriter has completed the review of your file, the Mortgage Consultant will receive a conditional approval. A conditional approval means your loan is approved subject to satisfying conditions (clarifying documents – see next step for more detail).

After your appraisal is completed you will receive an email from the appraisal network where you will be able to consent to eDelivery of the appraisal, download the authorization code, enter the code and then view the appraisal report.

Once your Processor has gathered all of the clarifying documents requested, they will submit them to the Underwriter for final approval. When the Underwriter gives final approval the Mortgage Consultant a clear to close, which means your loan can now close! At that time, your Processor will make arrangements with you and your Realtor to sign your closing documents at the Title Company.

You will need to review the closing disclosures 3 days prior to your closing and signing on the mortgage. Once you receive and review your closing documents, we must wait those mandatory 3 days before you are able to close.

Your final loan closing usually takes place at a Title Company with a Title Agent present to assist you with your documents. A closing can also be arranged to have loan documents signed remotely with a mobile notary. Your Realtor and Mortgage Consultant may attend your closing and help answer any questions you may have.

After you sign, it takes about 24-48 hours for your loan to fund and record. Your Processor will be working closely with the Lender and Title Company to ensure every “t” is crossed and every “i” is dotted. Once the loan has funded and recorded, you will receive your keys from the Realtor and can move into your new home. CONGRATULATIONS, you own a home!

“Shaun was a really helpful and detailed through the whole process of buying a home. He made it easy, let me know of anything I needed to close on the home. I would highly recommend Shaun to anyone who is in the market of buying a house. He will take care of you and help you through the entire process. Thanks again, Shaun!”

“First time buyer and couldn’t ask for a better experience. Shaun walked me through the steps and was able to purchase my home. He was available for any questions we had through this experience. Highly recommend Shaun and First Colony Mortgage!”

My wife and I had been looking to purchase our first home and we were somewhat nervous. Shaun helped us feel more confident and educated in our home purchasing decision. After our first interaction with Shaun, we could tell that he was experienced in the industry and he was able to explain everything clearly to us. Understanding the different steps to buying a home was very helpful and we would have been lost without the help of Shaun. We recommend using him and we also plan on using his services in future. Thanks Shaun!

This is our second time working with Shaun, and he is fantastic! He is thorough, efficient and hardworking. He kept us updated every step of the way. We had a few hiccups along the way due to our own credit history, but Shaun was patient through the process and when it all got sorted out he came prepared with several new options. One of which provided us with a lower rate than we were anticipating and lower closing costs. How can you ask for anything better? We would definitely recommend Shaun, and his expertise. We really enjoyed working with him again.

I am a first time home buyer! Shaun was extremely helpful throughout the entire process. He is knowledgeable, trustworthy, and took the time to make sure I thoroughly understood everything. Shaun was extremely responsive to all my questions, and would check in with me all the time. Shaun is truly the best! Thank you for help making my first home purchase experience so great!

Real clients discuss their real experiences during the home financing process

A little bit about us

NMLS# 3112

UT LIC# | 5492455

Loan Officer | NMLS# 1004093

![]()